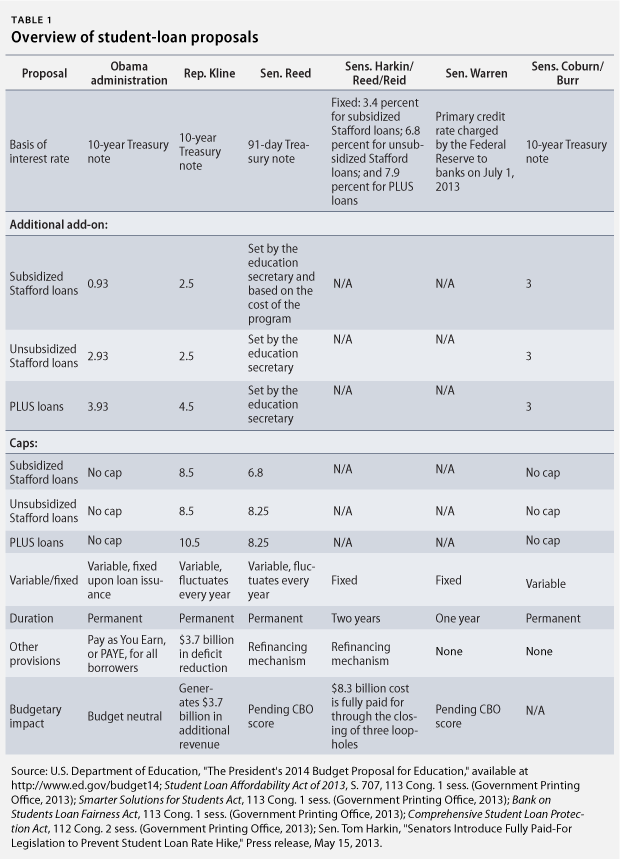

Alexander Holt

They’ve been reforms towards the Income-Created Repayment (IBR) program together with interest-100 % free work for into certain financing having undergraduates. This paper now offers a primary glance at the more than likely web effect of them alter suggested to have student and scholar students (excluding the results out-of removing the general public Services Mortgage Forgiveness system). I have fun with hypothetical debtor circumstances to compare exactly how much consumers which have additional loan balance create shell out within the Trump suggestion in contrast into established program. Essentially, we demonstrate that student youngsters create discovered an internet rise in professionals relative to the modern system due to earlier financing forgiveness. Men and women benefits was prominent to possess borrowers having above-mediocre expense and you can apparently large incomes when you look at the cost. The analysis now offers a note you to definitely graduate college students can found ample experts underneath the current IBR program without having to secure a low income. The newest Trump suggestion manage considerably dump professionals to own scholar youngsters lower than what they you will discover beneath the most recent IBR system as well as underneath the brand spanking new 2007 brand of IBR.

Addition

Specific individuals on federal financing system have obtained the choice and also make money-centered payments on their bills once the 1990s. But not, this choice try minimal inside extremely important indicates for many of the records and pair individuals tried it. Some alter ranging from 2007 and you will 2012 made this one incrementally so much more ample and accessible to every individuals. The changes helped alter the program out-of a tiny-utilized solution for the the one that a quarter out-of borrowers choose now. step 1 New borrowers regarding the federal education loan system because out-of 2014 may use the quintessential generous sorts of this method, today entitled Earnings-Based Installment (IBR), and this sets payments within 10 % off discretionary money and provides mortgage forgiveness your unpaid balance immediately after twenty years.

During the a promotion enjoy into the , then-presidential candidate Donald Trump revealed which he planned to allow consumers to pay a dozen.5 % of their earnings to your federal funds and discovered loan forgiveness immediately after 15 years. dos However it was not instantaneously clear if their suggestion manage increase otherwise slashed experts for individuals whilst manage additionally reduce just how long consumers will be needed to spend owed to before financing forgiveness while increasing brand new amounts they would pay monthly.

Chairman Trump reiterated so it suggestion when you look at the within a very detail by detail gang of reforms in his budget demand to Congress. 3 The information show that scholar pupils would certainly dump experts because of a unique 29-12 months financing forgiveness identity – right up on the newest 20-seasons forgiveness label. Borrowers in a few personal business operate could find the mortgage forgiveness title improved on loss of individuals Services Loan Forgiveness system, hence we beat due to the fact a different sort of benefit and you may exclude from our study. Whenever you are finances files reveal that the web effectation of the newest IBR proposal manage slow down the price of the borrowed funds program by $eight.6 mil a-year, one recommendations remaining open practical question regarding whether student youngsters carry out gain otherwise eliminate professionals. cuatro In fact, the newest funds additional a deeper side effects to this concern: they integrated a proposal to end the fresh new into the-college attract work for on a portion of fund for many undergraduates.

This report has the benefit of an initial look at the net effect of these transform getting undergraduate and you may graduate people and you may compares these to the existing IBR system.  We have fun with hypothetical problems examine simply how much individuals with different mortgage balances pay beneath the different words. Basically, we show that undergraduate people found an online rise in gurus in accordance with the modern IBR program on account of before loan forgiveness. In fact, the latest Trump proposition create create the most good income-founded fees system the federal government enjoys actually ever given student students rather than mention of the type of jobs they hold. 5 Scholar children, at exactly the same time, carry out located loan forgiveness in suggestion within infrequent cases, a major go from the modern IBR program. When you look at the share, the latest Trump proposition transfers benefits from graduate college students to help you undergraduates. Before proceeding compared to that analysis, it’s beneficial to discover some of the secret elements of the mortgage system.

We have fun with hypothetical problems examine simply how much individuals with different mortgage balances pay beneath the different words. Basically, we show that undergraduate people found an online rise in gurus in accordance with the modern IBR program on account of before loan forgiveness. In fact, the latest Trump proposition create create the most good income-founded fees system the federal government enjoys actually ever given student students rather than mention of the type of jobs they hold. 5 Scholar children, at exactly the same time, carry out located loan forgiveness in suggestion within infrequent cases, a major go from the modern IBR program. When you look at the share, the latest Trump proposition transfers benefits from graduate college students to help you undergraduates. Before proceeding compared to that analysis, it’s beneficial to discover some of the secret elements of the mortgage system.